Price development is not a one-way street

In the Netherlands of the 17th century, the investors already had to learn the difficult lesson that investments do not necessarily always move upwards in a linear way. It can be read that in 1637 the tulip bubble burst spectacularly after the price of a single tulip bulb had reached the same value as a grand canal house. Almost four hundred years later people do not seem to be any further or wiser.

Unimpressed by the past, people still have the understandable dream of accumulating considerable wealth (and to have it continually increased) with the least possible physical and mental effort and trouble, or, in other words, to earn money in their sleep. This is still what matters today. To this end, financial “jugglers” have a wide array of different approaches, legal and sometimes unfortunately not so legal, as seen by the Cum-Ex scandal in Europe.

In the present age, there have been various bubbles appearing, which have then burst: the dotcom bubble in 2000, the real estate and financial crisis in 2007/2008, the corona crash in 2020. And these will not have been the last bubbles. Whether a crypto or tech bubble will be spoken about in a few years’ time cannot yet be determined. We shall report on the many assessments further below.

However, it is not only stock and currency prices which are subject to speculative exaggerations as other asset classes are not immune, which tulips had already shown in years gone by. There were also probably other developments going on at the same time back then, but these are not as well documented and confirmed historically. Also, the real estate market, first in the USA (subprime) and then in China, has shown what can happen if it is effortless to be able to take part in considerable price hikes, above all with borrowed capital.

In this connection, it can easily be said that greed plays its part, or the fear of missing out on a mega rally. However, after a return to a healthy economic reality and people coming back to their senses, much of the economic momentum and value appreciation in the various sectors, which had been fuelled by speculation, is often undone again for a long time by a weak economic environment without any real growth.

Those who manage to get out of an overheated market in time are fortunate, realising a profit, and not only on paper, instead of accumulating significant losses. Here, the rather basic and often-cited (market) wisdom applies: “The money isn’t actually gone, it’s just in other pockets.” Indeed, a lot of money can also be made with bubbles. Certainly, where professional market participants are involved, who are well informed and very knowledgeable of the asset criteria. And who are prepared to work earnestly and also make courageous decisions.

However, as mentioned, this unfortunately only applies to some of the players. The warning signs of the recent rises in gold, silver and also the cryptocurrencies, followed by seemingly sudden and substantial corrections, should be heeded. And it should be taken note, that even the “banks for the little man and woman”, such as savings banks or cooperative banks, now allow the small saver to make investments in such as cryptocurrencies, which is quite fearful and worrying. Perhaps this means the pinnacle of the price trend has been reached, or is imminent.

Those who finish with losses are those who invest late in the market, in the firm belief of a presumably sure profit. However, the surest path to wealth is, and remains, in nearly all cases, through dedicated and professional work full of passion and enthusiasm. And if it is not even about riches, then the right timing and a little bit of luck always play an important part.

The nickel market looks a little different. This has just come through a long dry spell and is not in a bubble situation, although prices for consumers are naturally always too high. Nickel, or rather the nickel market, such as the London Metal Exchange (LME) and the Shanghai Futures Exchange (SHFE), is also not typically a playground for uninformed speculators and investors. This is because these specialised markets are much too small for large investors and volumes to also allow for a measured exit in every market phase. It is not, after all, the idea to drive prices down with one’s own sales.

Therefore, the metal interests of speculators are more drawn to precious metals, or perhaps even copper and aluminium, which will be examined in more detail later. Nickel certainly only plays second or even third fiddle. Yet, there is also investment interest in nickel, and even more important, in nickel as an alloy or battery metal produced in mines or as a recycled raw material. Therefore, the fundamental data of supply and demand have, in the medium term, an enormously important influence on availability and price development.

The outlook for 2026 seems to be basically good. Nickel was trading for a long time in a range between USD 14,500.00/mt and USD 15,500.00/mt before announcements were made in Indonesia (see below) which have now pushed prices higher. The high since the 1st January 2026 was USD 19,150.0/mt, the lowest level has been USD 16,500.00/mt.

But, like in previous years, the markets, not only for steel and stainless steel, were already firmly expected to move upwards “at least by the second half of the year”. That this did not happen can be seen today in economic data and company balance sheets. With the appropriate commercial caution it is, therefore, better to take things easy in 2026 and then a sustained more positive trend can be enjoyed. At the time of writing, the nickel price on the LME was around USD 17,000.00/mt.

Indonesia’s nickel policy moves the market – rally between hope and numbers reality

As already mentioned, the nickel market started the new year strongly. The reason was, and is, the expectation of many market participants that Indonesia – a heavyweight with its share of around 65% of global production – could limit the supply which had expanded strongly in previous years. The reaction on the LME clearly reflected this: The three months contract climbed from a low of around USD 14,200.00/mt mid-December to just short of USD 18,900.00/mt mid-January. A price level last reached in 2022.

The impulse for the trend change was an announcement from Indonesia’s capital Jakarta in December. The Energy Minister, Bahlil Lahadalia proposes to noticeably cut this year’s mining authorisations for nickel ore. The quotas are now expected to be between 250 and 260 million tons instead of the 379 million tons in 2025. In view of Indonesia’s dominant role on the world market, the market reaction was accordingly considerable.

However, there is a complex set of numbers hidden behind the headlines. The mining quotas are expressed in “wet tons”, which is inclusive of moisture content. According to analysts of Macquarie Bank, this can be as high as 40%, which makes it difficult to convert precisely into actual available nickel units, which are usually the reference in statistics and evaluations. In addition, there is a lack of transparency: Neither the actual mining quotas nor the actual production volumes are systematically published.

However, it can be confirmed that last year, the authorised volumes were already significantly higher than the actual demand. According to data from the Indonesian smelter group, FINI, demand for ore in 2025 was around 300 million tons. This also includes imports, above all from the Philippines, which, according to the World Bureau of Metal Statistics, reached about 14 million tonnes in the first eleven months.

FINI’s estimation for 2026 is a further increase in ore demand up to 340 to 350 million tonnes, since numerous processing plants will be powered up again. Therefore, even a reduced mining quota would not mean an abrupt cutback in supply, but more a gradual streamlining of the market. Current sources, such as Bloomberg on the 12th February 2026, emphasise that significantly higher nickel prices would necessitate a far tighter market. While copper’s visible warehouse stocks are actually at a low level, there is no trace of any significant reduction in nickel’s abundant reserves.

The Indonesian government is, above all, facing a balancing act. On the one hand, the excess supply should be contained and a sector, which has quickly grown in such a short time, has to be slowed down. On the other hand, existing plants, or the ones under construction, should not be held up by raw material shortages. With this in mind, Jakarta recently stopped the authorisation for new smelters for the production of nickel pig iron (NPI), which is primarily used in stainless steel production.

At the same time the government is tightening its stance against illegal mining and environmental violations. As J.P. Morgan emphasises, in January 2025 under President Prabowo Subianto, a task force was created solely for the enforcement of forestry and mining law, and is directly subordinate to the President. The aim is to systematically reduce illegal activities in forest areas, to regain state control and to generate additional state income. In the first year already, millions of illegally used hectares have been identified, licences have been rescinded and heavy fines imposed – a clear signal for a significantly harder regulatory course in Jakarta.

In addition, it has been announced that there will be a mid-year review of the mining quotas. Should supply and demand continue to diverge even more, then the figures could be adjusted once again. This means for the market: The current price rally largely reflects expectations – and Indonesia’s nickel policy remains a moving target. Also, the market has very often been misled by announcements which have then never actually been implemented.

Investors rediscover industrial metals – nickel drawn into the wake of the copper boom

The capital flows in the commodity sector are shifting noticeably. After precious metals almost exclusively profited from the so-called “debasement trade” in 2025, investors have now increasingly turned to base metals. Copper remains at the centre of this – yet nickel is also gradually being pulled in. If governments print more money, or run persistently high deficits, each individual monetary unit tends to lose buying power over time. Investors want to hedge against permanently higher structural inflation with a debasement trade.

Trigger for the movement was the decline of the US government bond yields in summer 2024. First to react was gold, silver later followed and finally also the industrial metals. While 94 percent of funds in ETFs (Exchange traded funds) flowed into precious metals last year, only 0.6 percent into industrial metals, but in January 2026 a clear change in trend was seen: In this month alone, the biggest industrial metal ETFs recorded inflows of 1.2 billion US dollars – more than the whole of 2025.

Copper remains the one to profit the most – the price recently rose to over USD 14,000.00/mt. On the LME, the net open interest (the total number of futures contracts that have not been closed out by settlement/countertrade at the end of a trading day), rose by 32.4 billion US dollars in 2025, whereby investment funds accounted for 21.9 billion. About half of these funds flowed into copper.

But the capital movement was not just restricted to the red metal. According to the breakdown of trading volumes by metal, activity increased significantly in 2026 for all base metals – explicitly including nickel. The strong volume push was especially noticeable at the beginning of the year, above all on the Shanghai Futures Exchange (SHFE) where the average daily volume in January climbed by 72 percent compared to the previous month.

The open interest on the SHFE also shows that nickel is part of this capital rotation. Here the aggregate open interest in base metals in 2025 rose by 20.3 billion US dollars. Nickel is listed as a separate component. At the same time, the 20 biggest futures houses reduced their net positions by 3.4 billion US dollars – an indication that new market participants and speculative funds could play a bigger role.

It is similar on the LME: While copper positioning dominates the trend, nickel is also part of the increased total engagement. The debasement trade has, therefore, not only affected copper, but also positively supported other industrial metals – even though not to the same extent.

However, as the capital flow increases, so does nervousness. The market for base metals is, as described above, relatively small – and in the meantime greatly visited. Chinese regulatory authorities have already reacted with stricter margin requirements, price limits and restrictions on high frequency trading in order to lessen exaggerations and to proactively ensure proper trading.

Artificial Intelligence (AI) in the spotlight

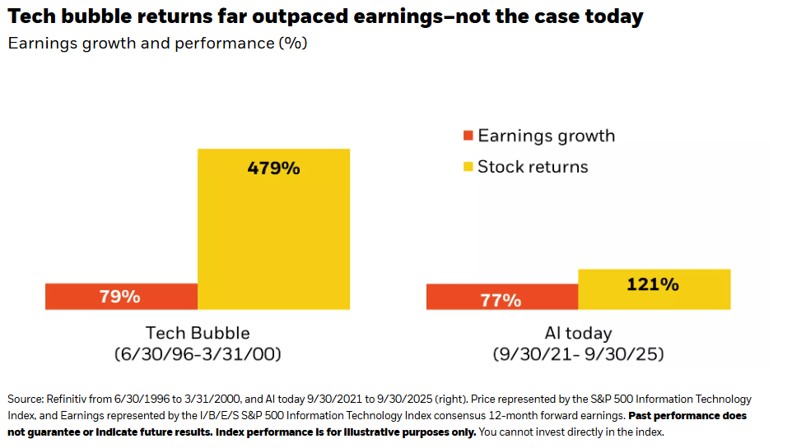

Artificial intelligence (AI) dominated the headlines in 2025, and this trend seems set to continue in 2026. Although AI is clearly transformative, from a technological and also social viewpoint, there is growing concern about the reviews and investment levels and many are questioning where the sector is possibly in a bubble phase.

The uncertainty is reflected in an October headline of Fortune magazine; “75% of profits, 80% of revenues, 90% of investments – AI has the S&P totally under control”, and the top analyst of Morgan Stanley is “very concerned”. While the headline was focused on the S&P, it is, however, applicable for the whole of the AI sector. The S&P is, after all, one of the world’s most important stock indices, which comprises of stocks from 500 leading listed US-American companies. Rapidly rising valuations and expenditures in the billions increase the fears of a bubble. These concerns are increased by the speed at which AI hardware quickly becomes outdated and by circular capital flows within the sector.

Howard Marks, co-founder of Oaktree Capital, highlights a similar momentum in his memo in December, with the title “Is it a Bubble?” (link). He points to speculative behaviour, the fear of missing out on something, circular business, special purpose entities and start-up capital rounds totalling 1 billion dollars, as signs for a bubble. He also notes that earlier transformative technologies – such as the combustion engine, radio and the internet – had bubbles which then burst, causing investors to suffer huge losses. However, the invested capital was vital for the development and launch, and these technologies eventually led to long-term productivity and social gains.

As far as productivity is concerned, the economic effects of AI remain uncertain, since it will possibly be restricted by overriding factors such as tariffs and geopolitical tensions, which have already characterised 2025 and global growth. Analysts of Macquarie Bank, amongst others, argue that productivity gains in the past lagged behind the introduction of transformative technologies, while the exact drivers of these gains remain controversial.

Despite strong arguments for an AI bubble, there are also prominent opposing arguments. The sector has more than a billion users, and hyperscalers (major providers of cloud-computing services) continue to show a strong turnover growth. In context, Goldman Sachs notes that AI-related investment expenditure is about 0.8% of GDP, compared to top values of 1.5% of GDP or more in earlier technology booms during the past 150 years (link). The valuations of AI-exposed stocks also remain well below those, which were seen in the recent real estate and internet bubbles (link). However, investment banks also have a considerable self-interest in these investment sectors.

LME (London Metal Exchange)

| LME Official Close (3 month) | ||||

| February 13, 2026 | ||||

| Nickel (Ni) | Copper (Cu) | Aluminium (Al) | ||

| Official Close 3 Mon. Ask |

17,010.00 USD/mt |

12,825.00 USD/mt |

3,028.00 USD/mt |

|

| LME stocks in mt | ||||

| January 13, 2026 | February 13, 2026 | Delta in mt | Delta in % | |

| Nickel (Ni) | 284,148 | 287,088 | + 2,940 | + 1.04% |

| Copper (Cu) | 141,550 | 203,875 | + 62,325 | + 44.03% |

| Aluminium (Al) | 494,000 | 481,550 | – 12,450 | – 2.52% |